🚐 20-Year RV Loan Calculator

Calculate monthly payments, total interest, and amortization for your 20-year RV loan

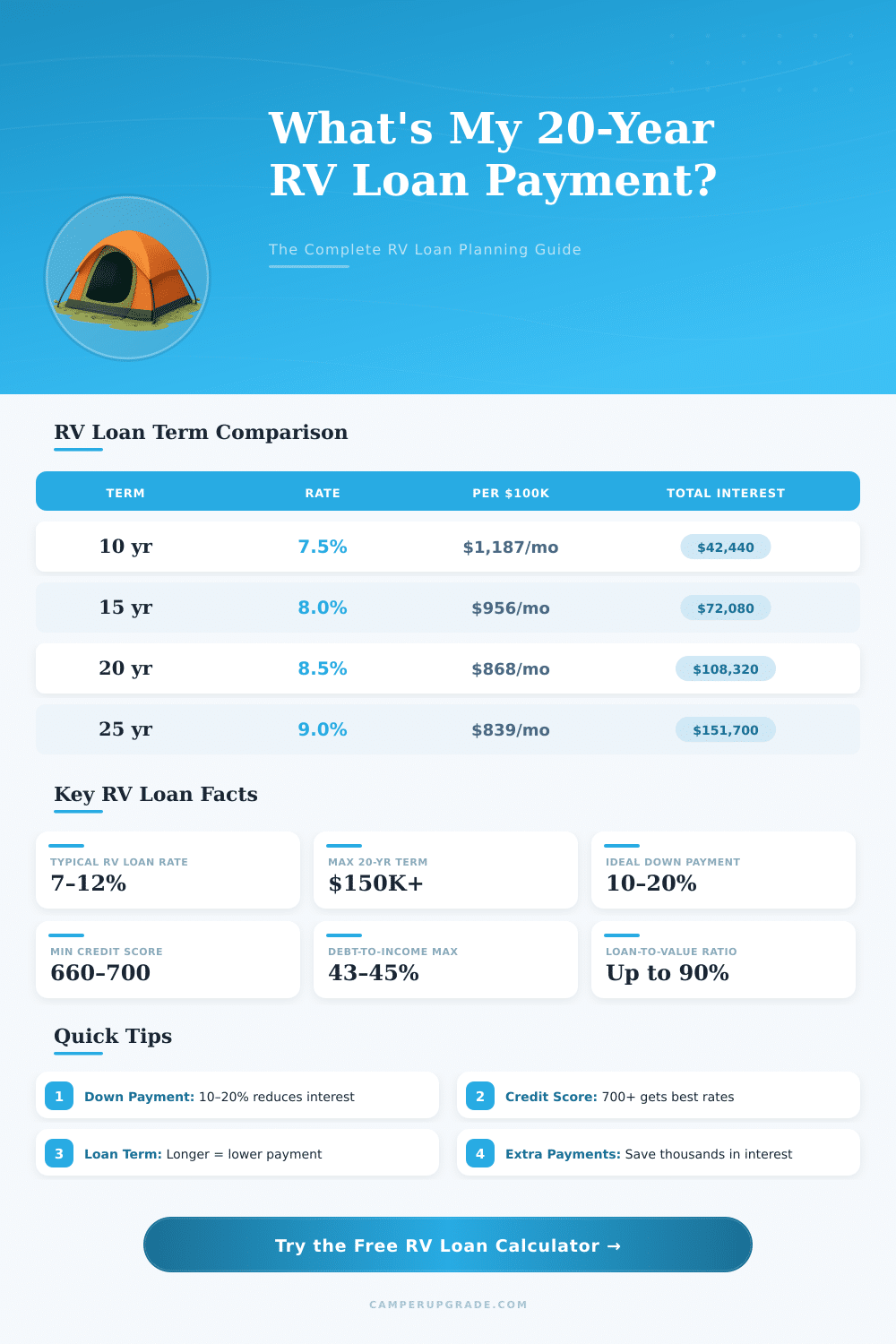

* Per $10,000 of financed amount. Multiply by your loan amount divided by 10,000 for an estimate.

| Term | Rate (Example) | Mo. Payment* | Total Interest* | Total Paid* |

|---|---|---|---|---|

| 10 Years | 7.50% | $1,187 | $42,436 | $142,436 |

| 12 Years | 7.75% | $1,064 | $52,960 | $152,960 |

| 15 Years | 8.00% | $956 | $72,080 | $172,080 |

| 20 Years | 8.50% | $868 | $108,320 | $208,320 |

| 25 Years | 9.00% | $839 | $151,700 | $251,700 |

* Based on $100,000 loan amount. Rates are illustrative averages; your rate will vary by lender and credit profile.

| RV Type | Typical Price Range | Typical Loan @ 10% Down | Est. 20-yr Payment @ 8.5% |

|---|---|---|---|

| Pop-Up Camper | $10K – $25K | $9K – $22.5K | $78 – $195/mo |

| Travel Trailer | $20K – $60K | $18K – $54K | $156 – $469/mo |

| Fifth Wheel | $40K – $120K | $36K – $108K | $312 – $937/mo |

| Class C Motorhome | $60K – $150K | $54K – $135K | $469 – $1,172/mo |

| Class B (Campervan) | $80K – $180K | $72K – $162K | $625 – $1,407/mo |

| Class A Motorhome | $100K – $400K | $90K – $360K | $781 – $3,125/mo |

| Toy Hauler | $30K – $130K | $27K – $117K | $234 – $1,016/mo |

| Down Payment | % Down | Loan Amount | Monthly Payment | Total Interest |

|---|---|---|---|---|

| $0 | 0% | $80,000 | $695/mo | $86,656 |

| $8,000 | 10% | $72,000 | $625/mo | $77,990 |

| $12,000 | 15% | $68,000 | $590/mo | $73,658 |

| $16,000 | 20% | $64,000 | $556/mo | $69,325 |

| $24,000 | 30% | $56,000 | $486/mo | $60,659 |

Whether you plan to fund a RV instead of pay everything upfront? Here the advantage of loan for RV: it allows you to sit behind the wheel of a motorhome, camper van travel trailer or fifth wheel, without fully emptying your bank account. The setup is like that of a car loan, but funding of RV usually lasts more long.

Various lenders bid terms until 180 months, so around 15 years. Because RV sometimes count as housing and not only as transport, it is possible to fund them even during 20 years. Even so, note that: used RV models commonly limit to around 10 years, and if the vehicle already is a bit old, extending the contract to 15 years can cause problems.

How to Get an RV Loan

Finding a loan for RV is not hard… You have several options. Banks, credit unions, online lenders and approved stores all offer financial help.

Credit unions commonly give more friendly rates, even so worth comparing, because one union maybe bids low rates for cars but hihg for RV, while another does the opposite. Here the key: some lenders work only in certain states or limit the mileage and model year, what can block your plans.

Stores also help with funding. When you buy at a dealer, they search for a good loan threw a net of lenders. Some dealer nets connect to more than 300 lenders, including big national and little local.

If you already have ties with a trusted union, the store can process the loan for you directly.

Getting approved before starting shopping is a very wise step. The process is fast: meet a loan adviser, sign a purchase contract, and usually everything ends in around 15 minutes. A down payment of about 20 percent helps a lot, and truly, the bigger deposit you give the lower rate you receive.

Loans for RV do not reach the flexibility of mortgages when dealing about rates. Some received 11 percent rates, others a rate of 9.24 percent through a store for a 180-month period. In better cases, credit unions deliver rates between 4 and 5 percent.

Here the tender part: long terms make the monthly payment noticeably lighter, but count the whole interest. You risk to pay twice more than the original amount for something, what is worth only half of its starting price at the end of the loan.

The loan amounts differ according to lender. Some start at only 1,500 dollars, others go until 20,000 or more. One bank allows clients a loan until 50,000 dollars directly, if the RV is not at a partner store.

Note that: above 100,000 dollars, the approval can getharder.

Loans for RV usually are not transferable. The lender rated the original request according to your credit score, your deposit and your signature. Not anyone else.

Hence, choosing a short period of four until six years truly will pay itself. You will escape years of extra interest that always builds when you stretch the time too long.